Fact Check

In an interview with Aruna newspaper, MP Godahewa made two claims: (1) the increase in tax revenue by 70% in the 2023 budget compared to 2022 is not practical, and (2) the tax hike has resulted in a 70% reduction in the income available for taxpayers to spend on their needs.

To verify these claims, FactCheck.lk consulted the Annual report for 2022 by the Central Bank of Sri Lanka (CBSL)

Claim 1: The MP’s claim that a 70% increase in tax revenue is impractical is incorrect for three main reasons.

First, increases in tax revenue result from (a) inflation and growth, when nominal wages and prices rise, the tax collection rises with it; and (b) policy changes, when the tax rate and people subject to tax rise tax collection rises also. The 70% increase in taxes for 2023 was projected as practical based on average (not the 12-month inflation reported) inflation being 29.9%, along with policy changes that could increase income and consumption taxes by more than 50% even without inflation. This shows that the expected increase was not impractical (see Exhibit 1).

Second, the MP’s assertion that the tax net will not widen and therefore require the increase to be borne by existing taxpayers is also incorrect. Two changes widened the income tax net: (i) lowering the income tax exemption threshold from LKR 3 million annually in 2020 to LKR 1.2 million in 2023. (ii) bringing in new taxes such as the Withholding Tax (WHT) on various forms of income, which otherwise could have eluded the tax net.

Third, the MP’s focus only on income taxes is also misplaced. Tax revenue is also derived from various other taxes, including Value Added Tax (VAT) and excise taxes, which fall under the category of consumption taxes. The majority of the increase in taxes for 2023 is expected from changes to VAT, rather than income taxes.

Claim 2: The MP’s claim that the increase in taxes led to a 70% reduction in the income available to taxpayers for their essential needs is also inaccurate for two reasons.

First, as shown earlier, the full increase in taxes is neither achieved through income taxes nor from the same people already paying taxes.

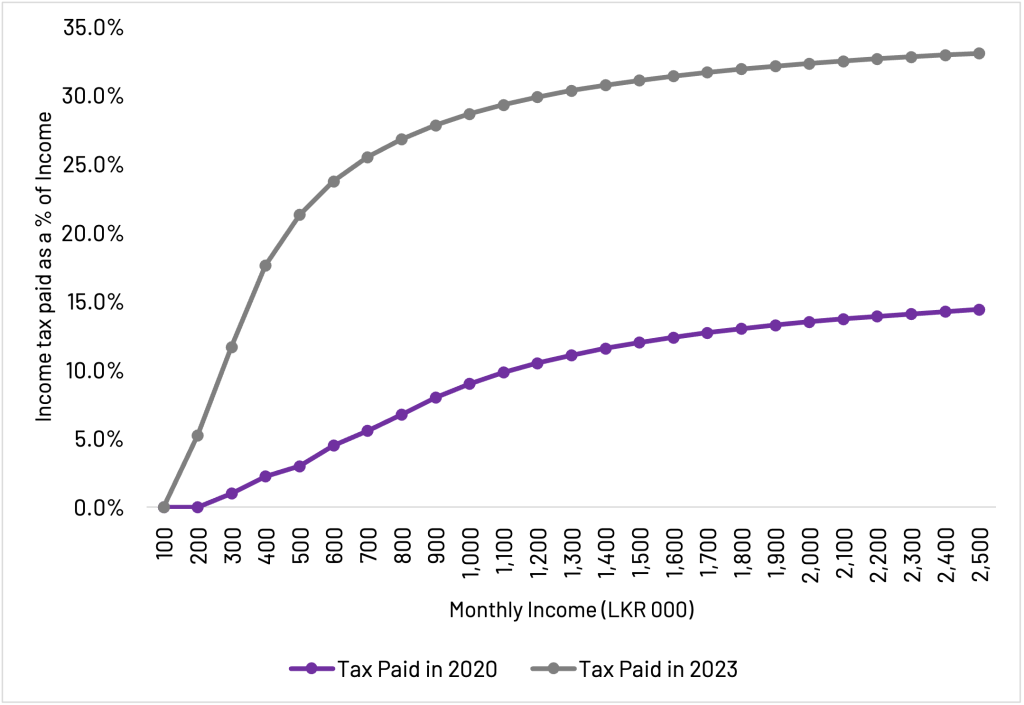

Second, the MP’s claim that a 70% increase in taxes paid would lead to a 70% reduction in disposable income is mathematically incorrect. For example, if an individual earns LKR 1,000 and pays LKR 100 in taxes, a 70% increase in tax payment would raise it to LKR 170. This would reduce post-tax income by 7%, not 70%, as claimed by the MP. The largest percentage change in income tax was for those earning LKR 800,000 a month, where disposal income would reduce from 746,000 to 585,500, which is a reduction of 22%, not 70%.

Overall, the MP is incorrect in both his claims. Therefore, we classify the MP’s statement as FALSE.

*FactCheck.lk’s verdict is based on the most recent information that is publicly accessible. As with every fact check, if new information becomes available, FactCheck.lk will revisit the assessment.

Exhibit 1: Increase in tax revenue from 2022 to 2023

Exhibit 2: Proportion of income tax paid as a percentage of income

Sources

Annual Reports 2022, Central Bank of Sri Lanka. https://www.cbsl.gov.lk/en/publications/economic-and-financial-reports/annual-reports/annual-report-2022