Is the Sri Lankan Government at Risk of Over-Borrowing in 2024?

An Explainer by FactCheck.lk

In the post-presidential election period, there have been several claims regarding government borrowing. Some argue that borrowing is excessive, while others contend it is reasonable. There are also conflicting claims about whether most of the borrowing is allocated to cover the budget deficit or to repay debt.

These debates often stem from differing interpretations of the purpose, impact, and necessity of government borrowing. This FactCheck.lk explainer aims to clarify three key questions surrounding government borrowing in Sri Lanka, providing an evidence-based analysis to cut through the confusion.

Question 1: Why do governments borrow?

Governments borrow primarily for three reasons.

a. To finance its primary deficit

When a government’s expenditure (excluding interest payments) exceeds its revenue, the shortfall is called the primary deficit. This shortfall is covered by borrowing, thereby increasing the country’s debt in absolute terms.

b. To finance its interest payments on debt

Over time, the accumulation of debt from running primary deficits require the government to pay interest on that debt. When there is a primary deficit, all of these interest payments are also financed through borrowing. The combination of (a) interest payments on debt, and (b) the primary deficit is referred to as the budget or fiscal deficit.

c. To finance its maturing debt

In addition to financing the budget deficit, governments must also borrow to repay the principal amounts of debt when they mature. When there is a budget deficit, the government can only settle the obligations of maturing debt by refinancing it through new debt.

Together, these annual obligations to finance (a)the primary deficit, (b) interest payments, and (c) repaying principal on maturing debt—add up to the total amount that the government would need to borrow each year. This is known as the Gross Financing Need (GFN).

Question 2: How much was the government expected to borrow in 2024?

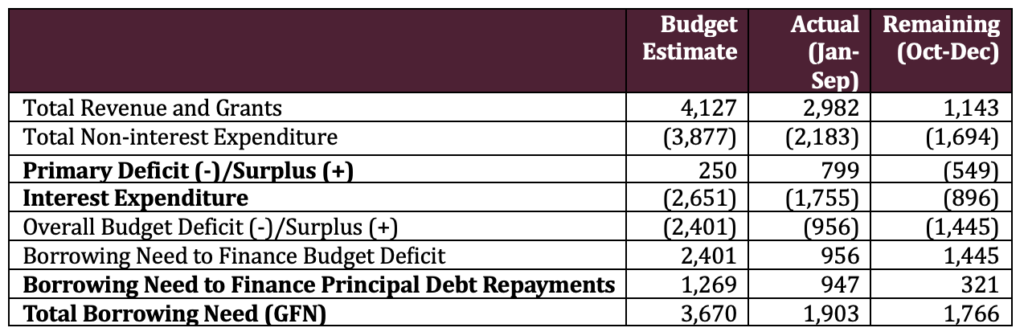

FactCheck.lk determined the government’s expected borrowing for 2024 by calculating the GFN. Exhibit 1 provides a breakdown of the GFN components and their respective data sources. It illustrates the methodology used to calculate the borrowing requirement, based on budget estimates and previously defined terms, and indicates a total GFN of LKR 3,670 billion (see Additional Note 1).

Exhibit 1: Government’s Borrowing Need for 2024 in Total (Figures in LKR billions)

Sources: Pre-election Budgetary Position Report and Report on Financial Performance of the Government up to third Quarter Ending 30th September 2024 published by MoF

Question 3: Will government borrowing for 2024 exceed expected borrowing?

In its budget, the government sets two borrowing expectations/limits for its:

(1) GFN (defined above), and

(2) debt stock increase – the total amount of debt the government owes at a specific point in time.

FactCheck.lk will test whether the government has exceeded its borrowing limits or remained within the expectations set for the year by evaluating domestic government borrowing against both of these limits.

GFN Test

Based on budget estimates, the government’s limit for GFN in 2024 was LKR 3,670 billion. MoF data shows that the actual borrowing for the first nine months (January to September 2024) amounted to LKR 1,903 billion. Therefore, there is another LKR 1,766 billion that the government can borrow during the final three months (October to December 2024), within the limit set by the budget.

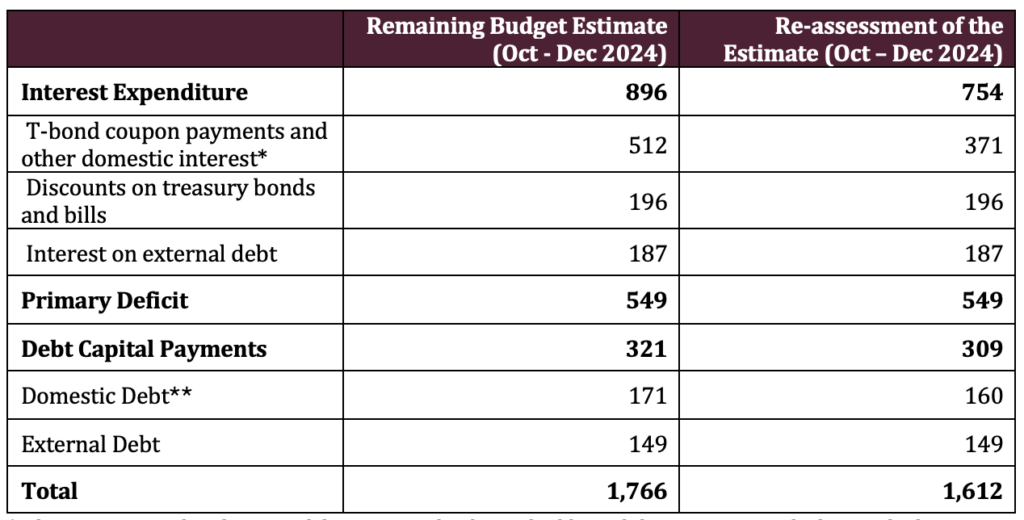

FactCheck.lk reassessed the estimated borrowing requirement for the period October to December 2024 based on available actual data. Our calculations indicate that the actual borrowing requirement for this period would amount to LKR 1,612 billion. This amount is lower than the LKR 1,766 billion (see Additional note 2 for details), and available within the budget limit. The reduced borrowing requirement can be attributed to reduced interest (coupon) payments on T-bonds compared to budget estimates.

Result: The borrowing for the year 2024 is not expected to exceed the budget limits set for GFN.

Debt Stock Test

To determine the expected limited on the increase of government debt stock, we subtract the expected debt repayments from the GFN limit.

If the government only borrowed to repay maturing debt, then the debt stock would not increase. However, in addition to that, if the government borrows to finance the budget deficit, it would then increase the debt stock.

Based on budget estimates for the year 2024, the government has projected a budget deficit of around LKR 2,401 billion and set an expected limit on the increase of the debt stock of about the same amount. During the first nine months (January to September 2024), the debt stock increased by LKR 956 billion. That means, the government still had LKR 1,445 billion for the last three months (October to December 2024) within the budgeted limit for increasing the debt stock.

The budget also sets out the expectations of how the borrowing to finance the deficit will be split between domestic and foreign borrowing. Of the balance LKR 1,445 billion left in the budget for the last three months, LKR 1,030 billion was expected to be financed by domestic borrowing, and LKR 415 billion from foreign borrowing.

From October to November 2024, domestic debt stock increased by LKR 371 billion. That means there was still leaving a more than ample LKR 659 billion within the domestic financing limits of the budget for the month of December.

Result: The ample borrowing capacity left in December demonstrates that the government’s total domestic borrowing in 2024 is well within the limits set in the budget.

The above results of government’s borrowing against the GFN limit, and increase in debt stock limit indicates that the government is not at risk of overborrowing in 2024.

Additional note 1: The approved budget for 2024 is LKR 7,350 billion. This total excludes the following allocations: LKR 3,000 billion for debt exchange under external debt restructuring, LKR 450 billion for bank recapitalization, and LKR 230 billion for adjustments related to the face value and cash value differences of government securities.

Source: Budget Speech for 2024

Additional note 2:

The treasury bond coupons and maturities are projected at LKR 371 billion, and LKR 160 billion as opposed to LKR 512 billion and 171 billion, respectively. Every other item of GFN is assumed to be the same as the budget estimates.

Exhibit 2: Re-assessment of the Budgeted Borrowing for October to December 2024 (Figures in LKR billion)

* The interest on other domestic debt is assumed to be negligible, and the assessment calculates only the treasury bond coupons.

** The capital payments on treasury bills are not accounted for in GFN calculation.

Sources: Pre-election Budgetary Position Report and Report on Financial Performance of the Government up to third Quarter Ending 30th September 2024 published by MoF, Central Bank Debt Statistics

Additional note 2:

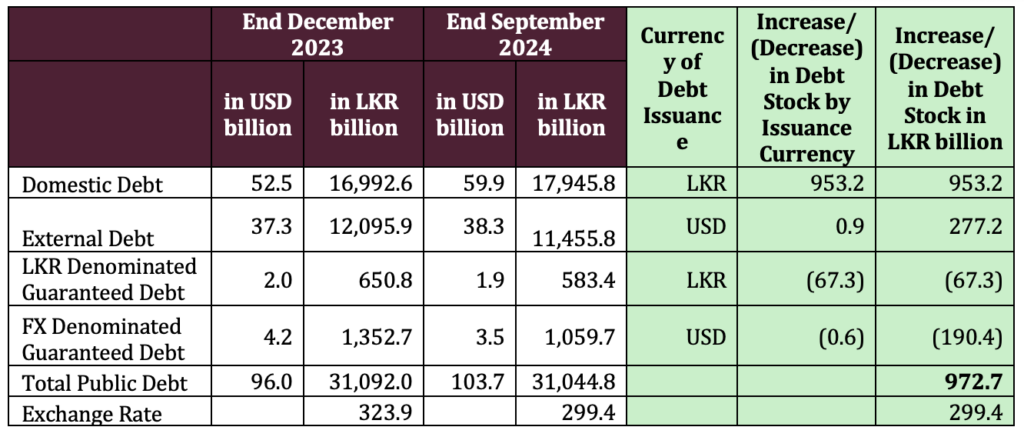

Exhibit 3 presents the public debt stock in both USD and LKR as of December 31, 2023, and September 30, 2024. It includes the changes in debt stock for each currency in which the debt is denominated and converts these changes into LKR for comparison with the budgeted figures.

The analysis calculates the nine-month increase in debt stock at LKR 972.4 billion, which closely aligns with the budget deficit of LKR 956 billion reported by the Ministry of Finance. This difference is due to changes in the exchange rate. This indicates that borrowing for the first nine months is consistent with the budget estimates.

Exhibit 3: Change in Public Debt Stock: End-December 2023 to End-September 2024

Source: The Quarterly Debt Bulletins published by MoF