Fact Check

Swasthika Arulingam, a candidate from the People’s Struggle Alliance at the 2024 General Elections, claims that Sri Lanka’s debt repayments under the restructuring agreement are higher than before the restructuring.

This claim is based on calculations that assume the entire debt restructuring follows the global option (see additional note) outlined in the September debt restructuring agreement with the bondholders, which preceded the final restructuring deal. Accordingly, to verify this claim, FactCheck.lk consulted the September debt restructuring agreement with Sri Lanka and the International Sovereign Bond (ISB) holders published by the Ministry of Finance and evaluated the claim on the global option.

Two key measures determine whether a country has effectively reduced its debt burden:

- Capital repayment reduction: Whether the total principal amount to be repaid has decreased.

- Interest reduction: Whether the interest rate on the interest payments per year have been reduced.

In Sri Lanka’s case, the September debt restructuring agreement had reductions in both areas.

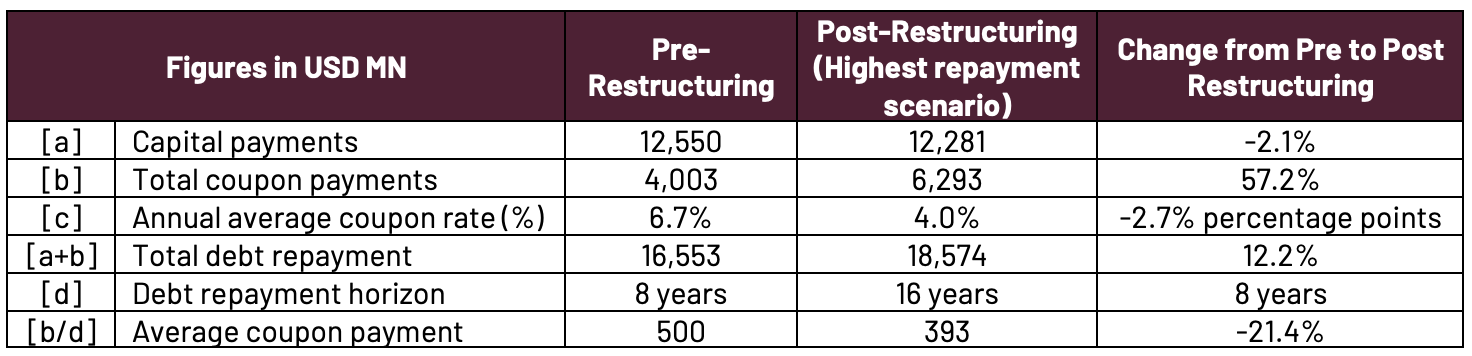

First, capital repayment was reduced compared to the original amount—from USD 12,550 million to USD 12,281 million (2.1% reduction). Second, nominal annual average interest payments were reduced from USD 500 million to USD 393 million (21.4% reduction). A more precise way to state the interest reduction is that the weighted average coupon (interest rate) reduced from 6.7% on the original capital to 4.0% on the agreed restructured (reduced) capital.

Additionally, the repayment timeline was extended from 8 years to 16 years, effectively doubling the repayment period.

Arulingam’s error is that she compares interest payments due over the extended repayment period against the interest payments that were due over the original shorter repayment period.

While it is the case that more will be paid in interest over 16 years than would have been paid in 8 years, this does not support the claim that the debt obligations were not reduced. Capital was reduced marginally, and the interest rate was reduced substantially relative to the interest rate on the original debt prior to restructuring.

Therefore, we classify Arulingam’s claim as FALSE.

*FactCheck.lk’s verdict is based on the most recent information that is publicly accessible. As with every fact check, if new information becomes available, FactCheck.lk will revisit the assessment.

Exhibit 1: Changes to International Sovereign Bond repayment before after restructuring

Source: London Stock Exchange, Ministry of Finance, Economic Stabilisation and National Policies, Verité Research Calculations

Additional note: Arulingam’s calculations exclude the local option, which was included in the final debt restructuring. At the time the claim was made, it was not possible to determine the take-up of the local option. Therefore, it is assumed that the entire debt restructuring follows the global option, and FactCheck.lk has conducted its calculations based on the same assumption.

[Updated 9 April 2025] Right of reply

FactCheck.lk responds to Swasthika Arulingam: Disagreement without a difference

This response addresses the contestations raised by Swasthika Arulingam in her official response published in the Daily FT newspaper on 2 April 2025 (see here). In her response, she cites the work and calculations of Dhanusha Gihan Pathirana, who also engaged with FactCheck.lk on social media (click here), sharing his own alternative spreadsheet calculation to contest our fact-check.

Our response will not engage with any tangential remarks or ad hominem attacks directed at FactCheck.lk or Verité Research or its employees by either Arulingam or Pathirana.

In her response, Arulingam begins by asserting the broader claim that the debt restructuring agreement was ‘disastrous for Sri Lanka’. The statement we fact-checked was a narrower, specific claim made within this broader context, arguing that Sri Lanka’s debt repayment terms under the restructuring agreement are more adverse than the pre-restructuring terms. Her full statement can be listened to here: https://www.facebook.com/watch/?v=2925672277609015 from 4:58 onwards.

FactCheck.lk reviewed Arulingam’s claim and found that both the capital repayment and the interest rate on debt was reduced by the restructured agreement, compared to the contracted terms that prevailed prior. As a result, FactCheck.lk evaluated Arulingam’s claim as false.

Since Arulingam cites Pathirana’s work as the basis for her claim, we will evaluate her response based on Pathirana’s analysis. We published an excel sheet with our calculations, which can be accessed here. Pathirana also provided his calculations on an excel sheet, which can be accessed here.

We want to begin by reiterating that despite the tonality of the engagement, we have taken Arulingam’s view seriously. We believe those we fact-check deserve the benefit of the doubt, and that their responses should be given the highest consideration. We also appreciate Pathirana’s engagement, as he not only presented his arguments but also by provided calculations that could be scrutinised, allowing us to response clearly.

Since Arulingam adopts Pathirana’s analysis, we consider addressing his arguments and calculations as an adequate response to Arulingam’s contestations of our fact-check.

Pathirana argues that the method used in our fact-check to calculate the interest rate and capital repayment reductions was inappropriate and that a different method should be used. We identified three specific points in which he disagreed, which we summarise, along with our brief responses, at the end of this reply.

It is not necessary to delve into the details of Pathirana’s disagreements to respond to Arulingam, because, despite differences in calculation methods, Pathirana’s results lead to the same conclusion as our fact-check: that both the interest rate and the capital repayment was reduced by the restructured agreement, compared to the contracted terms that prevailed prior.

This is seen in Pathirana’s spreadsheet: https://t.co/z0nBamQsW9.

(i) Cell E16 calculates pre-restructure interest rate as 6.95% and Cell B35 calculates the post-restructure interest rate (from 2028 onwards) as 6.81%, which is lower than the pre-restructure rate. He would get an even lower post restructure interest rate, if he calculated from prior to 2028 (but that has not been shown in his spreadsheet).

(ii) Cell E15 calculates pre-restructure capital repayment as USD 14,432 million, and Cell F31 calculates the post-restructure capital repayment as USD 12,278 Mn. Cell B36 notes that that the capital repayment has thereby reduced by 14.9%.

Pathirana’s methods (discussed further below) result in a smaller reduction in the interest rate and a larger reduction in the capital repayment than what FactCheck.lk calculated. However, his calculations explicitly show that both the interest rate and capital repayment have been reduced.

We hope this clarifies Arulingam’s concern regarding how her claim was evaluated. The evaluation based on the numbers she relied on is consistent with FactCheck.lk’s evaluation. The differences in the numbers are explained briefly below, though they are not material to the fact-check itself.

Further reading on the disagreements by Pathirana on the methods used by FactCheck.lk

Pathirana has argued that the method used to calculate the interest rate reduction and capital repayment reduction was incorrect, and that another method should be used. The specific points of disagreement are addressed below.

From Pathirana’s comments and calculations, we identified three main methodological disagreements with FactCheck.lk’s approach:

(D1) The effective interest rate calculation should not be the interest rate equivalent to the internal rate of return, but rather the average coupon payments weighted by capital on which those coupons are paid, and the duration of those coupon repayments.

(D2) The post-restructure repayment referred to as “past due interest” (PDI)—introduced to recover interest that Sri Lanka failed to pay between 2022 and 2024—should be counted as an interest payment, not as a capital payment; and

(D3) When comparing the two streams of repayment obligations, the pre-restructure stream should be evaluated starting from 2022, while the post-restructure stream should be evaluated only from 2024, and not from 2022.

FactCheck.lk’s evaluates these disagreements as follows.

- On D1 and D2 (disagreements 1 and 2): It is our view that the respondent’s alternative articulation points to an acceptable alternative method of making these calculations. However, there appear to be computation errors in the way these alternative methods were applied, which affect the results in his spreadsheet. That said, the idea that there are alternative methods to make these calculations is not contested. FactCheck.lk also checked its evaluation against various methods of calculation, even though the numbers were published in terms of just one method.

- On D2: We can explain the difference as follows: PDI is a calculation of capitalised interest that was due but not paid between 2022-2024. FactCheck.lk treated the capitalised component as payment of capital, and the interest on the capital as payment of interest. Pathirana argues that since it was past due interest from 2022, even the repayment of that capital component should be treated as an interest payment. We think both these treatments are acceptable. Pathirana’s treatment explains why his calculations result in a much larger estimation of the capital reduction (14.9%) compared to FactCheck.lk’s evaluation of the capital reduction as only 2.1%.

- On D3: We disagree with Pathirana’s view on two fronts. Firstly, both streams of payment should be compared from the same starting date for a like-for-like evaluation. Secondly, we think it is a contradiction to treat PDI as interest payments obligations from 2022-2024, as Pathirana does; and at the same time, assert that the payment obligations do not start in 2022.

However, as noted earlier, none of these disagreements (D1-D3) affect FactCheck.lk’s conclusion (or verdict), as Pathirana’s calculations lead to the same final result.

Sources

Announcement of Agreement in Principle, London Stock Exchange. https://www.londonstockexchange.com/news-article/70ZL/announcement-of-agreement-in-principle/16674142

Sri Lanka Reaches Debt Restructuring Agreements in Principle with External Creditors on Approximately US$ 17.5 BN of Sovereign Debt, Ministry of Finance, Economic Stabilisation and National Policies. https://www.treasury.gov.lk/api/file/16dc614c-d9a9-47ff-94d6-aab0811e62ba

Verité Research, https://mcusercontent.com/7dec08f7f8b599c6b421dfd10/files/b256b518-3858-9a6e-d8e0-c79598223cae/20250327_Verite_Media_DebtReduction.docx.xlsx