Fact Check

Minister Gunawardana justifies transferring expressways to a state-owned investment company to operate them as a “commercial enterprise” by arguing that: (a) Sri Lanka has borrowed LKR 800 billion in foreign loans to construct these expressways, and (b) it would take 160 years to repay the loans with the current annual profits (of LKR 5 billion).

To check this claim, FactCheck.lk consulted the Road Development Authority (RDA) Annual Report of 2021, the Ministry of Finance (MoF) Annual Report 2023 and statistics provided by the Department of External Resources Sri Lanka (ERD).

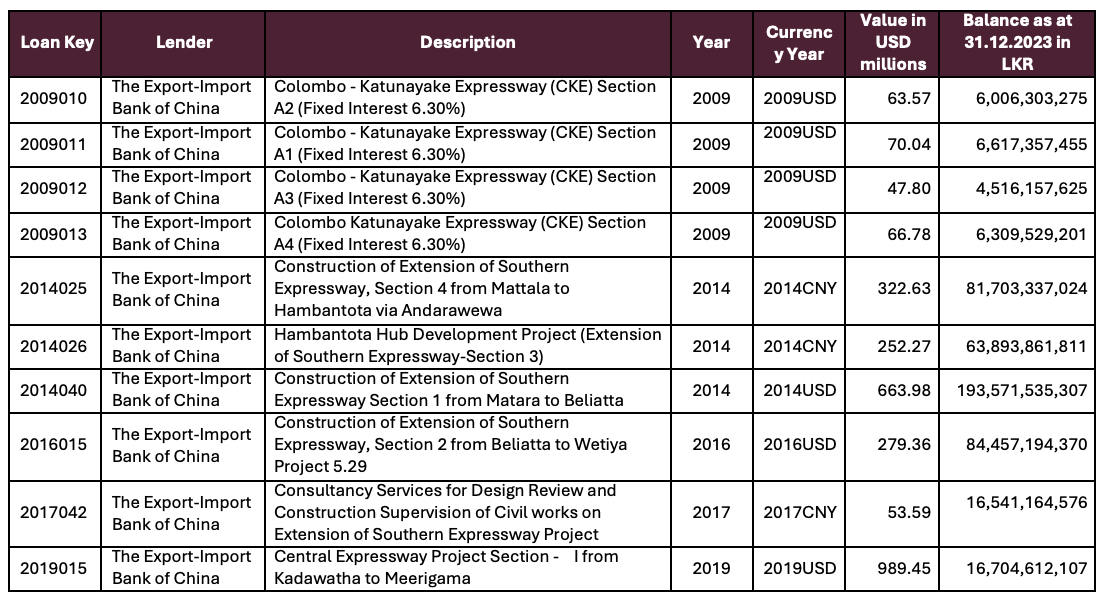

According to the MOF, as at 31 December 2023, the outstanding balance on all foreign loans for expressway development was LKR 480.3 billion, not the LKR 800 billion cited by the minister. (see Exhibit 1). The minister may have referred to the initial total value of these loans—USD 2,809.48 million (LKR 843 billion at USD 1 = LKR 300)—which has since been partially repaid.

The RDA reported that expressways generated a net income of LKR 4.5 billion in 2021. This is close to the LKR 5 billion figure cited by the minister.

The minister’s argument is that if Sri Lanka were to settle the balance using its annual profits from expressways, it would take approximately 160 years to settle the debt. He arrives at this figure by dividing LKR 800 billion by LKR 5 billion.

However, the logic in the minister’s calculation of the repayment problem is flawed in two ways. First, he assumes that annual profits will remain constant, ignoring potential growth from inflation and increased usage, which could lead to nominal growth of around 8.5% per year (with expected inflation at 5% and GDP growth above 3%).

Second, he ignores interest cost and currency depreciation in the loan settlement cost. The loans carry interest rates between 2% and 6.3%. Given Sri Lanka’s recent debt restructuring deal with its bilateral creditors, it is expected that outstanding debt will be restructured by approximately 30%. This would result in an average interest rate of 3%. Coupled with a depreciation rate expected to exceed 5%, the effective interest cost will be around 8%.

The above numbers indicate that even with restructuring of the debt and currency depreciation, the current income from highways is insufficient to service the interest cost (8% of LKR 480 billion is almost LKR 40 billion), let alone reduce the capital value of the outstanding loans. Therefore, the only way to repay the loan is to supplement the expressway income with funds from the treasury’s consolidated revenue.

The minister is hugely off the mark in supporting his argument. He incorrectly cites the outstanding loan balance as LKR 800 billion instead of LKR 480 billion, and his logic for calculating the repayment period using expressway income is also erroneous. However, even after correcting these mistakes, the challenge of repaying the loans from expressway earnings alone is more severe than he suggests. Despite his errors, the minister’s broader point remains valid: operating the expressways as a “commercial enterprise” could help ease the treasury’s debt servicing burden.

Therefore, we classify the minister’s claim as PARTLY TRUE.

Table 1: Outstanding Loan Commitments towards Expressways

Sources

Ministry of Finance (MoF) Annual Report 2023. Accessed via https://www.treasury.gov.lk/api/file/ad12f7fa-d2db-43d4-9daa-9270ee7b7cac

Road Development Authority (RDA) Annual Report 2021. Accessed via https://www.parliament.lk/uploads/documents/paperspresented/1704795000093592.pdf